When I first spoke to a fintech founder about the Digital Operational Resilience Act (DORA), his expression said it all—equal parts confusion and urgency. Despite being deeply technical and used to regulatory shifts, DORA had caught him off guard. That wasn’t surprising. Unlike other regulations, DORA doesn’t just sit quietly in the legal corner of operations; it reshapes how digital resilience is embedded into the heart of business strategy.

For fintech companies, especially those built on agile stacks and lean operational teams, compliance isn’t just about ticking a legal box—it’s about maintaining credibility in a market built on trust and uptime. So, what exactly does DORA require, and how can fintechs navigate it without breaking pace?

Let’s unpack the essentials and walk through the practical steps, challenges, and a full checklist tailored specifically for fintech firms navigating this new operational landscape.

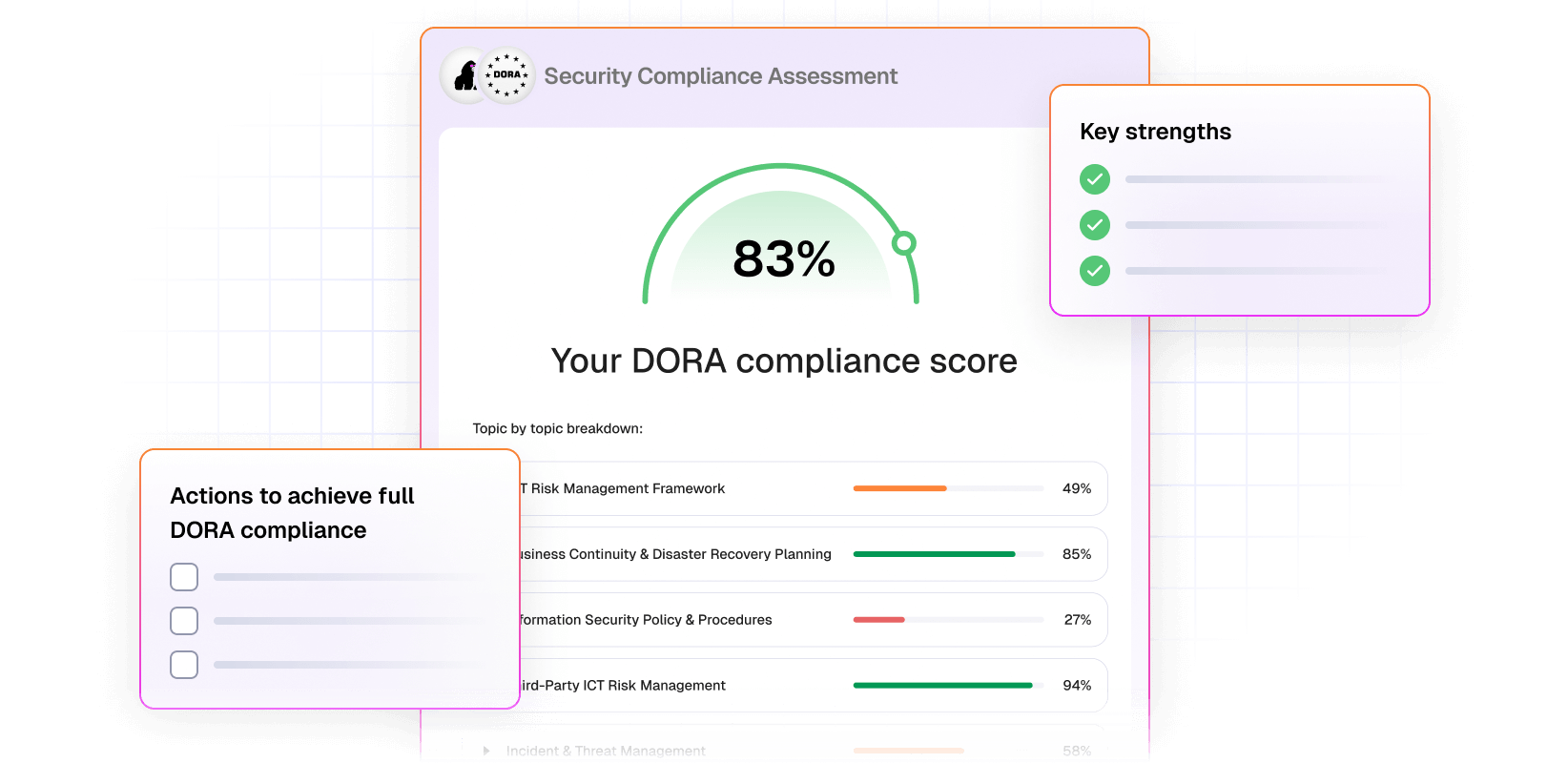

Assess your DORA readiness for free!

Evaluate your organization’s compliance gaps and find areas for improvement—no prior DORA knowledge needed.

Understanding DORA’s purpose in a fintech context

DORA was introduced by the European Union to ensure that all financial entities can withstand, respond to, and recover from all types of ICT-related disruptions and threats. Its scope includes banks, insurers, investment firms—and crucially, ICT third-party service providers, which many fintechs heavily rely on.

Unlike other regulations that target financial risk directly, DORA zeroes in on operational resilience, particularly how digital infrastructure and outsourced services are managed. For fintechs built on microservices, cloud-native stacks, and third-party APIs, this regulation hits very close to home.

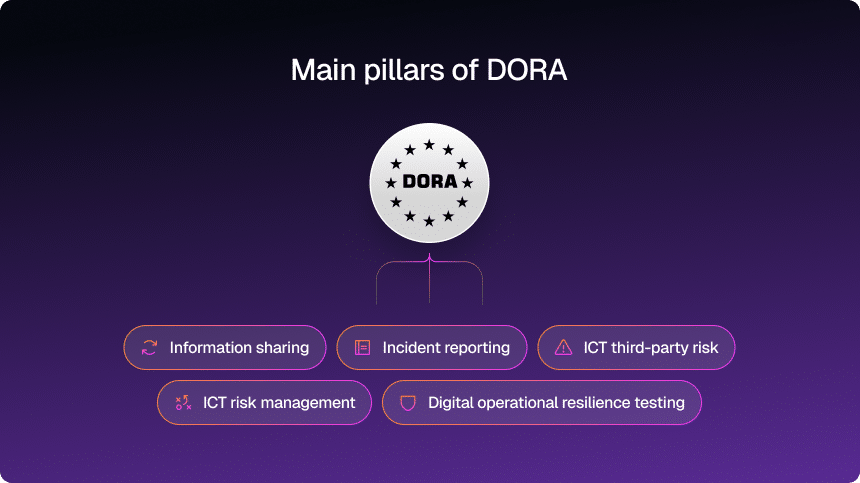

According to the European Commission, DORA aims to “consolidate and upgrade ICT risk requirements across the EU financial sector to ensure all participants are subject to a common set of standards.” This includes:

- Mandatory risk assessments of all ICT systems

- Oversight of third-party ICT providers

- Mandatory incident reporting with strict timelines

- Business continuity and disaster recovery testing

What does this mean in practice? Fintechs must not only secure their internal operations but also hold their vendors accountable—often in ways they haven’t done before.

PRO TIP

Build a service dependency map. Sketch out every API, microservice, and cloud component your fintech relies on. Label each by business-criticality. This visual will fast-track your DORA risk assessments and highlight single-point‐of-failure vendors.

Translating compliance into operations: fintech’s DORA checklist

Before diving into compliance execution, many fintech leaders ask me: “What exactly do we need to do?” The key lies in translating DORA’s five core pillars into clear, operational responsibilities. Below is a comprehensive checklist to help structure this journey.

The following table outlines the DORA compliance checklist for fintech businesses, organized by each core requirement.

| Core pillar | Requirement | Fintech action item |

| ICT Risk Management | Establish and maintain resilient ICT systems and tools | Map all ICT assets, conduct regular risk assessments, define protection and detection protocols |

| Incident Reporting | Report major ICT-related incidents within strict timeframes | Build a real-time incident tracking system, assign responsibility for reporting, align with ENISA guidance |

| Digital Operational Resilience Testing | Perform regular, threat-led penetration testing and scenario-based exercises | Conduct advanced red-team tests, simulate cyberattacks, validate backup and recovery processes |

| ICT Third-Party Risk | Identify and monitor all critical ICT providers | Formalize third-party risk assessments, update SLAs with resilience clauses, develop exit strategies |

| Information Sharing | Engage in voluntary threat and incident sharing initiatives | Participate in trusted intelligence networks and ISACs, define internal sharing processes |

Each of these action items isn’t just regulatory—it touches on how fintechs build reliability into their systems. After all, in a world where trust is increasingly tied to uptime and response speed, resilience becomes a differentiator.

Now that we’ve mapped out the responsibilities, the next challenge is execution—especially for lean teams.

PRO TIP

Automate your incident workflow. Integrate your incident tracking with Slack or Teams: use a “DORA Incident” tag that triggers a pre-defined response playbook (notifications, severity triage, regulatory reporting deadlines).

Adapting compliance to lean and agile teams

Here’s where I see most fintechs struggling: they’re designed for speed, iteration, and scale, not compliance overhead. So when DORA mandates extensive documentation, formal testing, and multi-party oversight, it can feel like dragging bricks through an agile sprint.

But the good news is that with the right approach, DORA can be integrated into existing DevSecOps pipelines and governance workflows. It doesn’t need to be a parallel world of bureaucracy. For instance, incident reporting mechanisms can be embedded into existing observability tools like Datadog or PagerDuty, while automated compliance logs can be generated through IaC frameworks.

Let’s break down some practical strategies fintechs can adopt to align with DORA without stalling innovation.

| Challenge | Tactical integration approach |

| Documentation and audit readiness | Use automated compliance platforms to collect and track evidence |

| Continuous testing for resilience | Embed testing scenarios into CI/CD pipelines using Chaos Engineering tools |

| Third-party visibility | Centralize third-party management in GRC platforms; sync vendor risk reports with contract tools |

| Rapid incident detection and response | Configure SIEM tools with custom DORA triggers |

| Communication and board-level reporting | Align reporting formats with NIS2 and DORA guidance, assign liaison roles across teams |

By embedding compliance into the tech stack rather than bolting it on, fintechs can meet DORA’s requirements while staying agile and focused on product growth.

But even with good systems in place, one area remains consistently risky: third-party dependencies.

PRO TIP

Embed resilience tests in CI/CD. Add a “blast radius” stage to your pipeline using Chaos Monkey or Gremlin. This ensures your build-and-deploy process itself validates DORA’s resilience testing pillar without manual effort.

Reassessing third-party risk under DORA

For many fintech firms, the real vulnerability isn’t internal systems—it’s in the black box of third-party providers. Whether it’s cloud platforms, data processors, or AI-based fraud detection tools, many of these vendors fall into the “critical ICT” category under DORA.

The regulation introduces direct oversight of third-party providers, meaning fintechs are now expected to enforce rigorous standards through their contracts and risk reviews. And this isn’t optional. Under DORA, entities must ensure they can exit from a third-party relationship without disruption—a tall order for those heavily embedded with hyperscalers or API service providers.

| Evaluation area | What to assess |

| Criticality of service | Is the service essential to business continuity or financial data operations? |

| Concentration risk | Do multiple critical services rely on a single vendor or jurisdiction? |

| Security & resilience posture | Has the vendor demonstrated robust security controls, SLAs, and incident response? |

| Contractual exit clauses | Can the business legally and operationally terminate the relationship cleanly? |

| Sub-outsourcing transparency | Does the provider disclose all subcontractors and chain of service delivery? |

This level of scrutiny may feel intrusive, but it reflects the growing understanding that systemic digital risks often lurk beyond the firewall. The fintechs that take this seriously will be better prepared when—not if—disruption strikes.

Make DORA work for your fintech—without slowing you down

DORA compliance doesn’t have to compete with your product roadmap. CyberUpgrade helps fintech teams embed digital resilience into daily operations—without adding friction. Our platform automates vulnerability scans, third-party risk reviews, and incident response workflows directly inside tools your team already uses, like Slack or Teams.

We eliminate 80% of manual compliance tasks with guided workflows, real-time evidence collection, and centralized audit readiness. That means no more spreadsheet chaos or missed deadlines—just a streamlined path to staying DORA-compliant while focusing on growth. Whether it’s updating SLAs, testing resilience, or managing vendor dependencies, our fractional CISOs help you navigate the complexities with confidence.

Our clients typically save over €60K annually compared to hiring a full-time compliance lead—and gain a future-proof security posture regulators trust. Let CyberUpgrade turn DORA into your competitive advantage. Book your consultation today.

Are you prepared for the next incident?

DORA isn’t just another piece of EU regulation. For fintech businesses, it’s a stress test for operational maturity. It challenges teams to start building resilience and long-term trust.

Many firms I’ve worked with found that once the initial fog of regulatory uncertainty cleared, DORA became an opportunity—a framework to tighten processes, rethink vendor reliance, and build a more transparent operational culture.

Fintech’s competitive edge has always been speed, but in today’s volatile digital environment, resilience is the new differentiator. As DORA’s enforcement phase unfolds, those who’ve done the hard work early will not only avoid penalties—they’ll earn the trust of users, investors, and regulators alike.

If your team hasn’t started preparing yet, now’s the time to ask: is your business architecture built to withstand the next disruption? Because DORA is no longer coming. It’s here.

Assess your DORA readiness for free!

Evaluate your organization’s compliance gaps and find areas for improvement—no prior DORA knowledge needed.